Financial Markets

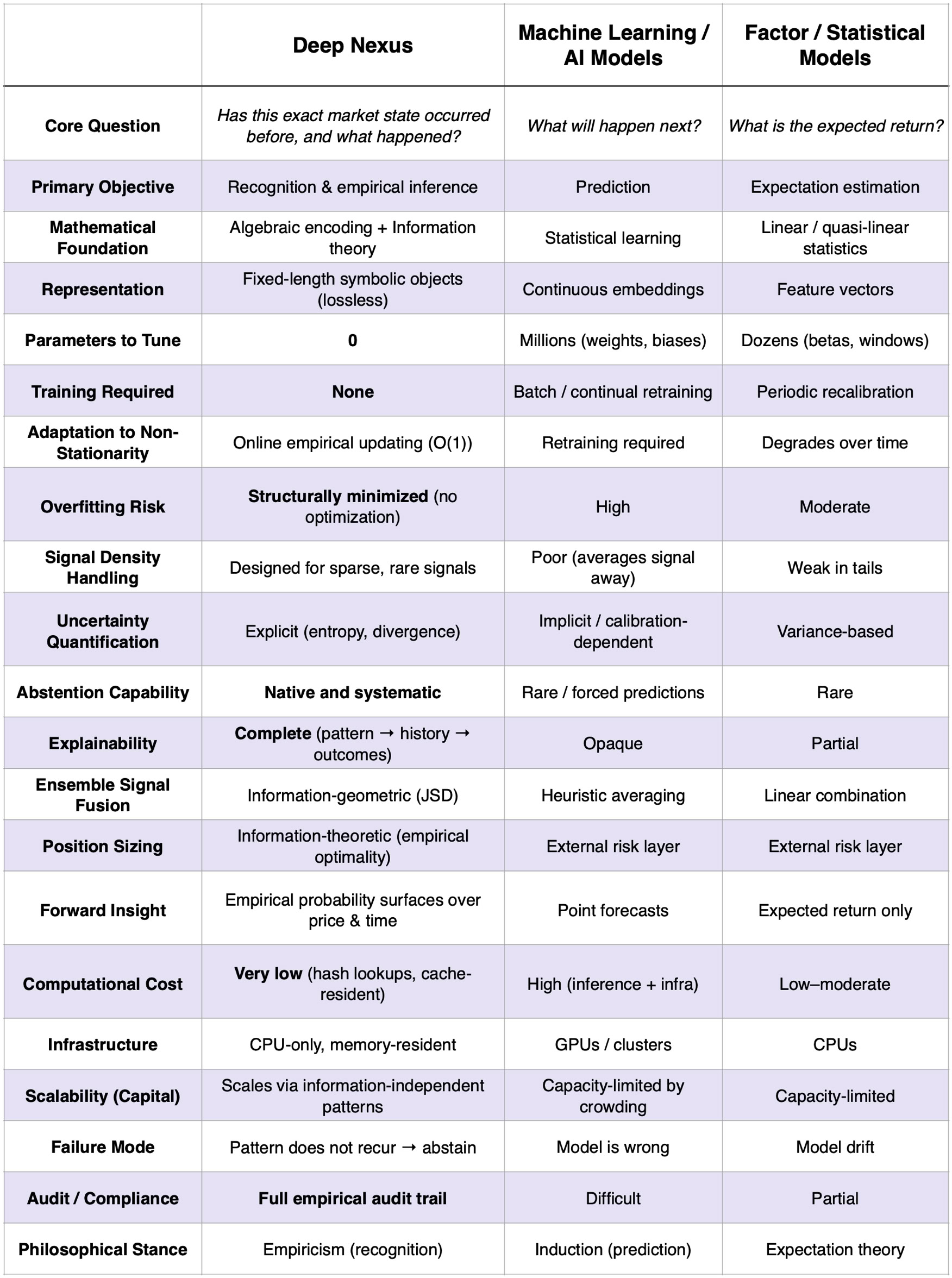

For financial markets, Deep Nexus has developed and implemented a deterministic, information-theoretic market representation and execution system.

Rather than predicting prices or returns, our systems map market state-space and empirically measure forward outcomes conditioned on historically identical patterns. The result is a fully deterministic, explainable market intelligence system that evolves through empirical accumulation without retraining, parameter optimization, or model decay.

Why Prediction Fails in Markets

Financial markets violate the core assumptions underlying most quantitative models:

• Non-stationarity: Statistical relationships change over time.

• Heavy tails: Returns are not normally distributed.

• Sparse signal: Observed data points do not all have equal value.

Machine-learning systems attempt to approximate continuous functions over this environment, inevitably fitting noise and smoothing away the very structure that produces outsized returns. Even well designed models often perform well in backtests but degrade rapidly out-of-sample.

Our framework does not rely on predictive modeling. Instead, decisions are based entirely on empirical recognition where structure is discovered, cataloged, and reused only when it reappears.

Research & Strategic Inquiries

The system for markets is currently operated for internal use. We may selectively engage with partners aligned with long-term system development.